Most people at one point or another have heard the strong opinions floating around about the healthcare system. Frankly, if you haven’t one quick look at the healthcare twitter hashtag will give you enough insight into people’s colorful views.

Health care is a right, not a privilege. We need Medicare for All so we can end the disgrace of 30 million Americans having no health insurance, and many more being underinsured with high deductibles and co-payments.

— Bernie Sanders (@SenSanders) January 2, 2019

Health care is not a right. Your rights do not come from government. https://t.co/rTpVbg8JO2

— Joe Walsh (@WalshFreedom) January 2, 2019

etc

Healthcare in the United States is a highly contested subject, everyone has an opinion whether it be passionate and aggressive or plainly casual. Though there are a variety of sentiments towards healthcare, a majority of people align themselves with politicians. Unfortunately the healthcare system tends to be a highly partisan issue. But it doesn’t have to be. The issue of healthcare, unlike most other partisan problems, starts from the same place no matter where the party lines divide. Healthcare is something every single person in the United States has some form of connection to, and it is something that most would describe as being deeply flawed. So what is the big issue? Well, not everyone understands or agrees on what is wrong with the system. This is where conflicts start to arise.

The United States’ healthcare system is incredibly flawed, it consists of many problems ranging from lacking affordability to outright corruption. These problems are bringing the American public to an understanding that it is time for something better. We’re beginning to believe it is time for change.

The United States needs an affordable universal healthcare system that ensures all Americans have access to efficient and functional services.

What is the system?

The Current System

The American healthcare system is incredibly complex, but at its’ core it is comprised of people, health insurance, healthcare providers, and manufacturers. The most important piece of the system being health insurance. There are many different types of health insurance in the United States the main ones being private insurance through employer, individual private insurance, the Veterans’ Administration, Medicare, and Medicaid. All of these systems provide care for their buyers, by covering medical costs under specific conditions.

Private insurance plans all function in similar manors, the buyers pay insurance companies what is known as a premium. A premium is a payment to the insurance company in exchange for coverage. Premiums are notoriously expensive and fluctuate based on the rest of the healthcare marketplace. In addition to premiums people will have what is known as a deductible. A deductible is the amount of money that must be paid out-of-pocket towards medical bills before insurance companies will step in. And even after the premiums and deductibles there are further specifications including additional fees for in/out-of network care, co-payments, and what medical procedures and medications the insurance will cover.

The other forms of insurance are the Veterans’ Administration, Medicare, and Medicaid. The Veterans’ Administration provides complete health insurance for veterans. They even provide nursing home coverage, which most other insurance plans don’t cover. The main problem with this program is that it is incredibly overrun, there are too many people who are entitled to coverage from them and not enough funding.

Medicare and Medicaid have similar problems. Medicare is a government system for everyone over the age of 65 who paid the Medicare tax or had a spouse who did. This system covers most healthcare expenditures; however, unlike the V.A. it does not cover nursing home costs. It also behaves more like a private insurance company with the specifications of what it will cover, but it is an insurance that is almost universally accepted. Medicaid like Medicare is a government system, but it is provided for people of extremely low income households. When someone is a part of the Medicaid program the government covers the cost of their insurance. Medicaid is less specific about what it will cover, but is only accepted by certain places as a form of coverage.

All of theses insurance systems work together to provide coverage for the American people; however, there are so many gaps that people fall through. Like the lack of affordability, the lack of funding, and the lack of regulation in the system

Why This System Doesn’t Work

The current healthcare system in America is failing for a multitude of different reasons. America spends more on healthcare than any other developed nation and despite this millions of people are unable to receive healthcare and/or insurance causing absurd levels of bankruptcy. And those who are able to access coverage may run into other cost issues due to the complexity of the system and insurance companies ability to manipulate it for profit.

The Flaws of the System

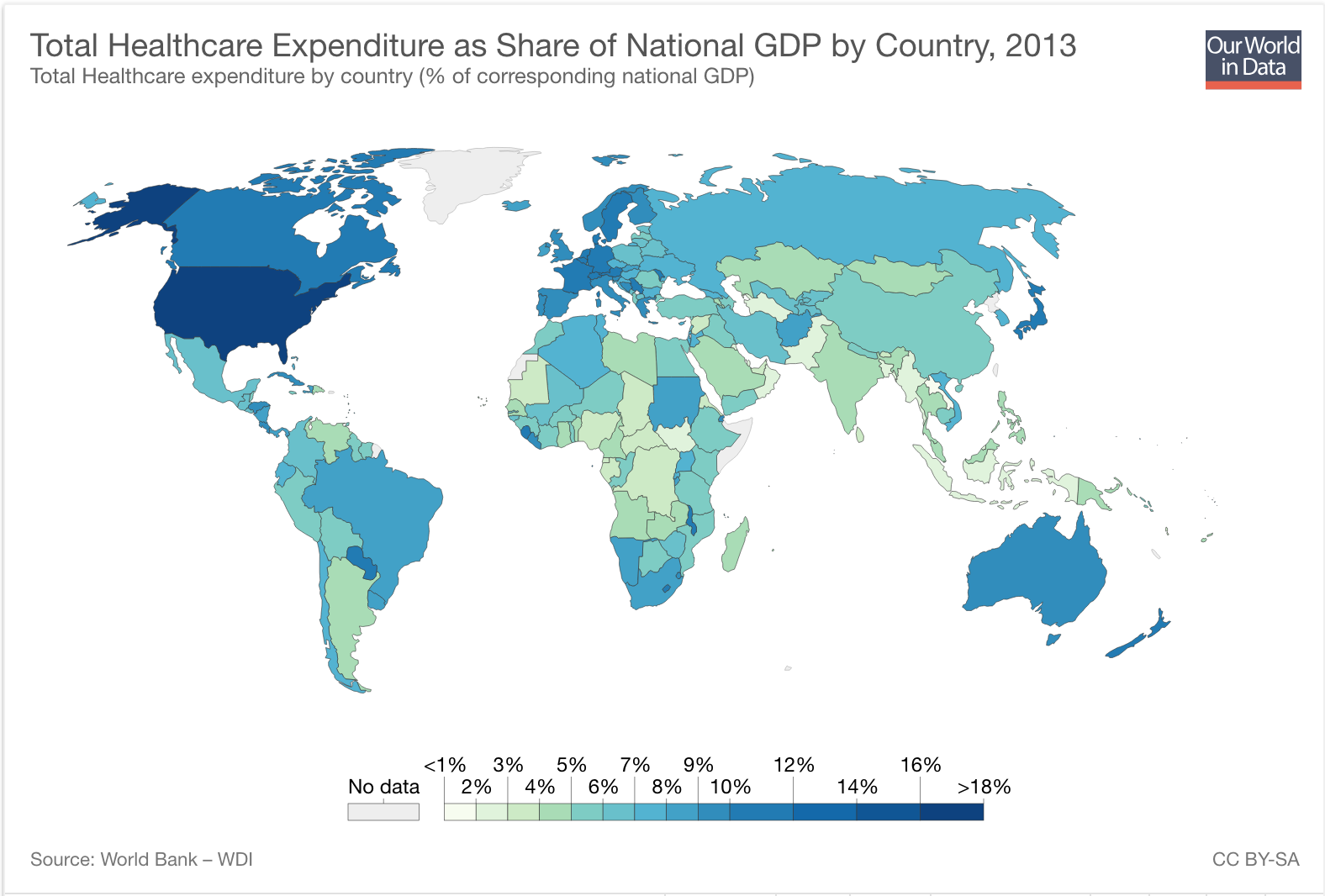

America Spends More on Healthcare Than Any other Developed Nation

[perfectpullquote align=”right” bordertop=”false” cite=”” link=”” color=”” class=”” size=””]”In 2016 America spends $10,348 per person on healthcare, roughly twice as much as the average for comparable rich countries”[/perfectpullquote]

America is one of the few developed nations in the world which has failed to implement a universal healthcare system. America’s staunch refusal and resistance to change has left the nation with an overly complex system and skyrocketing costs. An article by The Economist writes, “In 2016 America spends $10,348 per person on healthcare, roughly twice as much as the average for comparable rich countries.” These astronomical per person expenditures stem not from better quality or access to healthcare, but derive from the complex administrative system which exists in the United States, as well as insurance companies viewing healthcare as subordinate to profit. These higher costs also indicate a fragmented insurance market, which gives the average consumer little involvement in the overall healthcare process, and no ability to negotiate the prices of medical services. This explains the difference in prices of medical procedures depending on the insurer. The Economist explains further in one of their articles that having an appendix removed “can cost anywhere from $1,500 to $183,000.” These inflated prices are one of the major causes of the difference in spending between America and other developed nations.

Another reason for the large difference in prices is where the money is going. In the United States administrative costs are significantly higher than in Europe, NBC’s Blumberg reports, “Administrative costs[…] accounted for 8 percent of total national health expenditures in the U.S. For other countries, they ranged from 1 percent to 3 percent.” The United States is paying more for healthcare than any other developed nation, the main reason for this being the inflated prices of medical procedures and the outlandish, unnecessary administrative costs.

Lack of Affordability

[perfectpullquote align=”left” bordertop=”false” cite=”” link=”” color=”” class=”” size=””]”44 percent of adult Americans claim they could not come up with $400 in an emergency without turning to credit cards, family and friends, or selling off possessions. When this reality combines with healthcare bills the consequences can be financially devastating”[/perfectpullquote]

The price of insurance makes it difficult for many Americans to maintain a positive health insurance status and uphold financial stability. Private insurance comes with many financial obligations including premiums, deductibles, co-payments, out-of-network fees, and more. These requirements place a significant, and every increasing burden on American families. Regardless of their place on the income stratum. In fact, in a 2017 report by the Consumer Financial Protection Bureau stated, “medical debt was the most common reason for someone to be contacted by a debt collector.” Why is this the case? Well according to a study by the Kaiser Family Foundation in 2016 “half of all insurance policy-holders faced a deductible […] of at least $1,000.” And for those who purchase their health insurance through an Affordable Care Act exchange, the fee will be even greater: “90 percent [of consumers] have deductibles of $1300 for an individual or $2600 for a family.” These deductibles may not sound like a huge expense; however, an annual survey called the Report on the Economic Well-Being of U.S. Households by the Federal Reserve Board concluded that “44 percent of adult Americans claim they could not come up with $400 in an emergency without turning to credit cards, family and friends, or selling off possessions. When this reality combines with healthcare bills the consequences can be financially devastating.” If most Americans cannot produce $400 in an emergency, then they most certainly cannot fork over thousands of dollars to fill their deductible. In addition these prices are stacked on top of all other household expenditures and insurance premiums. Sometimes insurance companies will also have out-of-network fees on top of everything else. Meaning if medical care is received outside of an insurance companies’ parameters, they will not consider the money spent on that care as part of the deductible payment.

An example of someone who was financially challenged by the system is a man named Daniel McCarthy. Daniel is a middle class working man who had a nursing position at his local nursing home and rehabilitation center, when his four year old daughter Cassidy was diagnosed with cancer. McCarthy was devastated and he had no way to pay for the reported “several thousand dollars in out-of-pocket medical expenses- for the surgeon, the anesthesiologist, radiologist, chemotherapy, [etc].” And the only reason he had to was because of the family’s “$6,000 deductible.” To add insult to injury McCarthy lost his job, forcing the family to find money for the few thousand dollars a month COBRA payments on top of everything else. The United States Department of Labor defines COBRA as a system that “gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan.” The saving grace of the McCarthy family was the nonprofit called the Heather Pendergast Fund, who knew about the McCarthy’s because of Daniel’s habitual volunteering at a local fire department. The organization was able to cover a majority of the McCarthy’s overall expenditures. Some aren’t as lucky as the McCarthy family, Daniel himself even said, “I don’t know how people who don’t have the resources do this. I don’t. Many people work three, four jobs, and can’t afford the time to volunteer in an organization like the fire department that would be able to help them. There are many people living out there that need help that can’t find it.” There are many people just like the McCarthy’s who need help. People who need help from the financially crippling healthcare system that lacks contingency plans.

Insurance Companies Control Too Much

Insurance companies’ ability to decide specific procedures and which pharmaceutical drugs they will or will not cover forces many Americans to either neglect their own care, or spend tremendous amounts of out-of-pocket payments. For example, a high school student by the pseudonym, Eli Carlos, lives in pain because he is unable to pay for a necessary knee surgery. Eli was hiking on a vacation with his mother in Wisconsin, and while he was walking he stepped wrong and permanently hyperextended his knee. This continues to cause him extreme pain while doing everyday activities such as walking, running, and swimming. It is possible for Eli to alleviate this pain if he were to receive Arthroscopic surgery; however, his family’s private insurance through his father’s employer does not cover it. Meaning, his family would have to pay anywhere from $3,000 to $16,000. This is very unmanageable with Eli’s household income. So due to Eli’s insurance companies’ decision to not cover Arthroscopic surgery, Eli must live in pain until he is able to pay for the procedure himself. Eli’s story is not uncommon. There are many stories just like his.

Another example being Doctor Kevin R. Campbell, a cardiologist who has experienced the difficulties of an insurance company refusing coverage for a pharmaceutical drug he needed. Doctor Campbell tried for months to find the right medication to treat his high cholesterol. He tried many different drug cocktails until he finally found one that worked, Crestor and Zetia. Campbell remained on these drugs for another 18 months with the best results possible, until his insurance company decided to stop coverage for Crestor. Campbell immediately protested this, telling the company he had already tried many different medications, none of which worked. Despite this his insurance company told him to find another drug, Campbells said, “This left me with two choices that I suspect many of my patients have faced in the past: either pay out of pocket- to the tune of nearly $500 per month – for my drugs, or simply go untreated.” There are so many people who experience this everyday. Insurance companies’ decisions about what they will or will not cover forces people to go without care or pay obscene amounts of money.

The People Without Insurance

[perfectpullquote align=”right” bordertop=”false” cite=”” link=”” color=”” class=”” size=””]”Today 10% of Americans below retirement age are without insurance”[/perfectpullquote]

Millions of American citizens live without health insurance coverage due to its’ lack of affordability. The combination of inflated prices, and skyrocketing insurance premiums, makes it nearly impossible for some to have health insurance. An article by The Economist estimates, “Today 10% of Americans below retirement age are without insurance.” The 10% most likely do not have insurance because they fall between the gap of those who can afford private insurance, and those who qualify for Medicaid. Or they have been affected by healthcare costs rising faster than the average wage. The issue of the uninsured affects everyone, even those that are insured. In fact, the number of uninsured people directly affects the cost of insurance premiums, which is a significant issue because it may push more people into being uninsured.

The issue of the uninsured raising the price of insurance premiums is a particularly heated topic between Democratic and Republican politicians. The debate surrounds the Affordable Care Act or the ACA. The ACA contains a mandate stating that all people are required to have some form of insurance. Otherwise they will pay an ever increasing fine that will eventually be more costly than the price of insurance itself. Republican politicians want to repeal this mandate along with most of the ACA; however, and article from the New York Times states, “Insurance companies and Democrats in Congress find themselves in rare agreement, predicting that premiums will soar and insurance market will swoon if the government can no longer threaten people with tax penalties for going without health insurance.” If something isn’t done about the repeal of the ACA to either prevent it or replace it with a genuinely better system then insurance premiums will skyrocket and the number of uninsured people will increase.

There are many other reasons to be against having millions of uninsured Americans, but the increase in the cost of healthcare for everyone is definitely the most notable.

Overall the System is Broken

The American healthcare system is incredibly flawed; prices are inflated for profit making the entire system unaffordable. It forces many people to live a life of pain and discomfort, and leaves millions of people without proper healthcare, despite the belief of high quality care. These systematic errors have been a problem for years, and it is time that the American people stand for their rights to quality affordable healthcare and recognize the politicians who are willing to push for it.

What is a Possible Solution?

A possible solution to America’s healthcare problem, is what is known as a single-payer universal healthcare system. This is a system that has been adopted by a multitude of other developed nations such as Canada, The United Kingdom, Finland, Australia, and Iceland.

What is Single-Payer Universal Healthcare?

Single-payer universal healthcare (SPUHC) is a healthcare system that provides insurance coverage for all the citizens of a nation through a single public agency. Typically through the government.

What Would It Do?

Single-payer universal healthcare would simplify the complex American system, it would provide insurance coverage for everyone, spending could be better controlled, and best of all it may save the average working American a lot of money.

SPUHC would provide coverage for every American. The system would essentially be like Medicare for all. Except it would have significantly more funding, because all people would be required to pay into the system, proportional to their gross paycheck. According to Reuters News Agency SPUHC is, “a publicly financed, privately delivered system will all Americans enrolled and all medically necessary services covered.”

[perfectpullquote align=”right” bordertop=”false” cite=”” link=”” color=”” class=”” size=””]“Universal health coverage would be a major step towards equality, especially for uninsured and underinsured Americans. Overall expenses and wasteful spending could be better controlled through cost control and lower administrative costs, as evidenced in other countries”[/perfectpullquote]

SPUHC would remove unnecessary spending and promote more efficient use of the money Americans spend on healthcare. It would simplify the incredibly complex system in the United States, which is rife with inexplicable costs and administrative spending not found in the systems of other developed nations. The supporters of SPUHC say, “Universal health coverage would be a major step towards equality, especially for uninsured and underinsured Americans. Overall expenses and wasteful spending could be better controlled through cost control and lower administrative costs, as evidenced in other countries.”

A majority of the arguments against SPUHC posit that such a system would require an unacceptable increase to income tax rates; however, an article by NBC states, “Most Americans would find any tax hikes offset by savings on household health-care costs.” In other words, the amount saved by not paying premiums, co-payments, or necessary medical care previously uncovered by insurance would cover any additional tax liability required to pay for SPUHC. Other nations like Canada have already proven these benefits to be true NBC reports, “Canada has successfully implemented a single-payer system even though Canadians pay about the same amount in taxes as Americans.” Now some may argue that Canada’s healthcare is lower quality to that in the United States; however, that isn’t entirely true. According to a study, analyzing 11 high income nations, by the Commonwealth Fund in 2017 “[t]he performance of Canada’s system ranked ninth, […] while the American health-care system ranked last.” The United States would significantly benefit from, at the very least, adopting a similar system to Canada, if not something better.

[perfectpullquote align=”left” bordertop=”false” cite=”” link=”” color=”” class=”” size=””]“70 percent [of Americans], now support Medicare-for-all, otherwise known as single-payer healthcare”[/perfectpullquote]

In addition to all of the positives of a single-payer universal healthcare system, a majority of Americans already support it. According to a Reuters survey “70 percent [of Americans], now support Medicare-for-all, otherwise known as single-payer healthcare.”

Why Doesn’t the U.S. Have This System?

There are many different speculations as to why the United States hasn’t adopted a single-payer healthcare system. The most common thought as to why the U.S. doesn’t have this system is that the political opposition is far too strong. Think about it, an article by The Economist says, “9 out of 10 best paid occupations involve medicine, doctors have little incentive to change the system.” The people with most power have no incentive to change anything. Doctors aren’t the only ones who are opposed to it. In a Harvard analysis other stakeholders include “health insurers, organized medicine, and pharmaceutical companies” because they are the ones with the most to lose.

The real reason why Americans aren’t able to access healthcare is because there are too many powerful political opposers not willing to make the change.

What is the solution to this? Who knows. But the important thing to take away from all of this is that Americans have a right to a better more efficient and affordable healthcare system. It is about time that they take advantage of this right.

Featured image by Darko Stojanovic